National Inventory Rises 4.6% Year-Over-Year but Pace of Growth Cools

Active housing inventory across the United States climbed 4.6% from April 2025 to April 2026, reaching 1,002,935 listings, according to Realtor.com data analyzed by ResiClub. However, this marks a sharp slowdown from the 30.6% year-over-year surge recorded just 12 months earlier.

“The rapid inventory gains we saw in 2024 and early 2025 are now leveling off,” said Dr. Emily Torres, senior housing economist at the National Real Estate Analytics Group. “This suggests the pendulum of power is no longer swinging sharply toward buyers, but instead settling into a more balanced but still tight market.”

Despite the increase, national inventory remains 11.8% below pre-pandemic April 2019 levels—a persistent shortfall that continues to underpin price resilience in many regions.

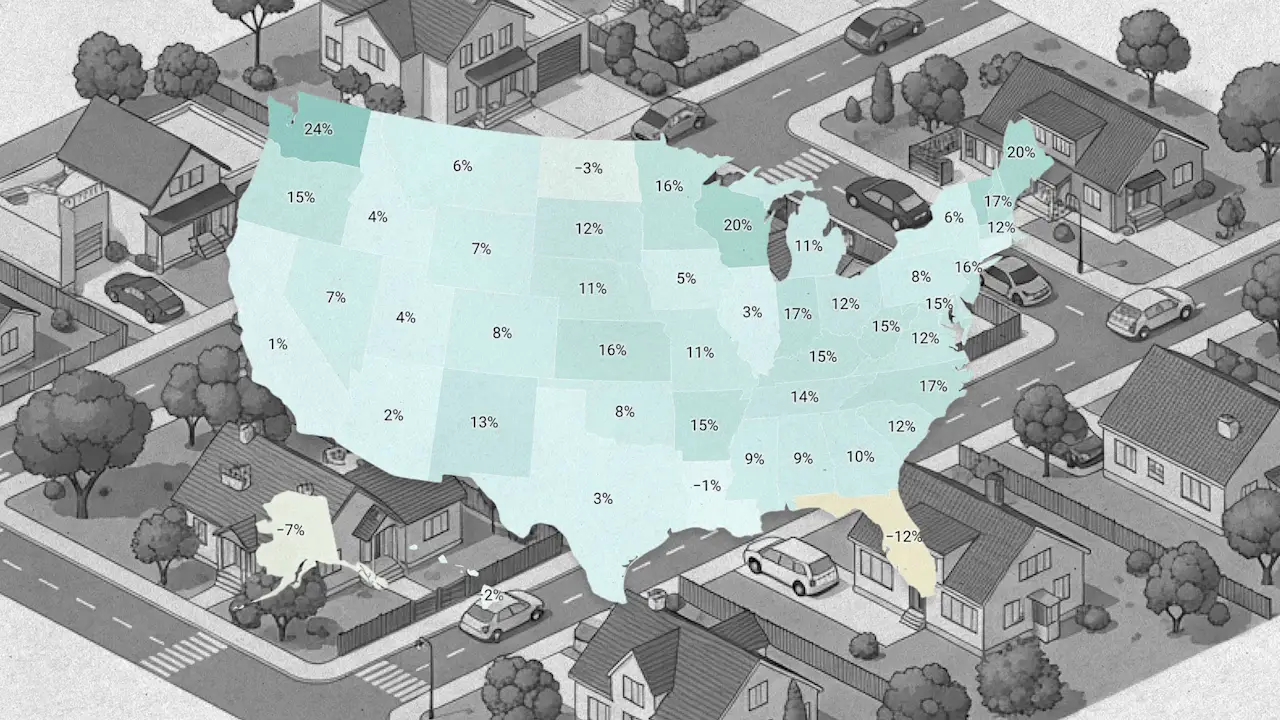

Power Shift Varies Widely by State

Since the pandemic housing boom peaked in 2022, the overall market has seen a directional shift from sellers to buyers. Yet that transition is far from uniform across the country. States with inventory now above 2019 levels—such as Florida, Texas, and Arizona—have experienced softer home price growth or outright declines over the past 47 months. In contrast, states like New York, Massachusetts, and California, where inventory remains far below pre-pandemic levels, have seen more resilient price appreciation.

“In markets where listings have surged past pre-pandemic benchmarks, buyers are finally gaining leverage to negotiate on price and terms,” said Jason Lin, chief economist at the Housing Market Institute. “But in the Northeast and parts of the Midwest, sellers still have the upper hand because of acute supply constraints.”

Active Listings by State: A Tale of Two Markets

ResiClub’s data ranks states by year-over-year inventory change, highlighting the stark divergence: inventory-rich states like Colorado and Nevada posted double-digit increases, while inventory-poor states like Vermont and Maine saw declines. The median months of supply—a key measure of market balance—remains below 4 months in tight markets, signaling continued seller dominance.

Background: Why Inventory Matters for Prices

ResiClub monitors active listings and months of supply to gauge home price momentum. A rapid increase in listings, coupled with longer time on market, often signals pricing softness—or even weakness. Conversely, a sharp drop in listings beyond normal seasonality suggests sellers are regaining control.

Since 2022, the national dynamic has tilted slowly toward buyers, but the pace of that tilt is now decelerating. The year-over-year inventory growth rate has fallen from 30.6% to 4.6% in the span of 12 months, indicating that the market is finding a new equilibrium.

What This Means for Home Shoppers and Sellers

For buyers: In states where inventory has surged, such as Florida and Texas, there are more options and less competition—creating opportunities to negotiate. However, in still-tight markets like the Northeast, buyers face limited choice and elevated prices. “The window of buyer leverage is narrowing in many places,” Torres cautioned. “Act soon if you’re seeing favorable conditions.”

For sellers: The days of easy price escalation may be over, especially in inventory-rich states. Pricing competitively and preparing for longer marketing times is essential. In tight markets, sellers can still command strong premiums, but even there, growth is moderating.

Nationally, the trajectory over the next year hinges on whether the current pace of inventory adds continues. If it does, the market could approach 1.05 million listings by April 2027—still below 2019’s 1.14 million, but a significant step toward balance.

Key Takeaways

- National active inventory up 4.6% year-over-year (April 2026 vs. April 2025)

- Growth pace has slowed dramatically from 30.6% the prior year

- Inventory remains 11.8% below April 2019 pre-pandemic levels

- Power balance varies: buyer-friendly in inventory-rich states, seller-friendly in tight markets

- Historical comparison: April 2019 inventory was 1,137,198 vs. 1,002,935 in April 2026

To see the full state-by-state breakdown, visit ResiClub’s interactive map.